By Alex Conley

Rate Cuts vs Reality – Navigating Retail CRE’s Next Phase

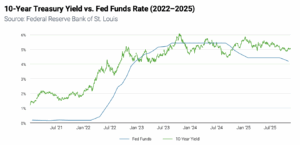

After nearly two years of monetary tightening, the Federal Reserve delivered its second consecutive 25-basis-point rate cut on October 29, lowering the federal funds rate to 3.75%-4.00%, the lowest level since 2022. The move confirmed the start of a gradual easing cycle and was accompanied by another major announcement: the Fed will end its balance-sheet reduction program (Quantitative Tightening) on December 1. A positive sign for real estate markets long term.

Markets had largely priced in the rate cut ahead of the decision. Proven by the 10-year Treasury rising above 4% the day before and after the rate cut. The S&P 500 hit record highs, but Powell’s hawkish-leaning tone reminded investors that policy would remain data-dependent.

In this article, I’ll outline how these shifting macro forces are impacting retail deal flow — and what investors should be focused on right now

A Market Defined by Uncertainty — and Adaptation

In recent weeks, nearly every conversation I’ve had with investors—whether managing directors at public firms, private equity professionals, or individual owners — has centered on one theme: uncertainty. Not simply over just rates, but over what the next six months of fundamentals will look like. Even Peter Linneman, who has built a career on clear market calls, recently admitted on the Webcast that he has “no strong take” on where the macro or micro environment heads from here. When economists of his stature step back from conviction, it underscores how opaque this moment feels.

That said, as John Chang of Marcus & Millichap and Kyle Matthews of Matthews Real Estate have both emphasized in recent LinkedIn posts, we now understand this market. We know its boundaries, its challenges, and how to navigate them. Transactions are still happening — in fact, more than in the previous two years — because investors have learned to get comfortable operating within today’s parameters, even if it’s not yet a market of comfort.

Why the Rate Cuts Haven’t Moved the Needle — Yet

The Fed’s overnight rate is only one piece of a much larger puzzle. In commercial real estate, the 10-year Treasury yield remains the key benchmark for pricing debt. Although the Fed has cut twice, the 10-year has traded between 3.9% and 4.1%, reflecting long-term concerns around federal borrowing, inflation durability, and global demand for U.S. debt. The real headwind is uncertainty, not the absolute cost of capital.

For CRE borrowers, lending spreads remain elevated as banks continue to price conservatively amid tighter regulations and constrained liquidity. The end of quantitative tightening should begin to relieve this pressure by reducing one of the main forces that has kept long-term rates higher. The lending environment is far from easy, but it’s finally becoming predictable.

Cost of capital has modestly improved over the past six months, but lenders remain extremely conservative in their underwriting and deal execution. The biggest constraint continues to be loan-to-value ratios, with few transactions closing above 60%. Banks are cautious to add exposure — what appears to be 60% leverage today can turn into 80% if values or property performance shift unexpectedly.

The Bid-Ask Spread Remains the Market’s Defining Friction

Even more than debt costs, the bid-ask spread between sellers and buyers continues to define the slow transaction volume of the past two years. Sellers, many of whom refinanced in the ultra-low-rate era, remain anchored to 2021 pricing. Buyers, facing higher leverage costs and stricter underwriting, require yields that justify the risk.

A common concern among buyers has been, ‘Why should I invest in a 6% yielding real estate asset when I can earn nearly 5% from a government-backed Treasury bill or bond?’ While real estate offers distinct advantages such as tax benefits, appreciation, and inflation protection, this yield comparison has remained a meaningful psychological hurdle in today’s market.

As George De Rossi wrote in Leveraged Breakdowns, “When bond yields rise, real estate’s attractiveness as an investment option declines… buyers require a higher yield for the same risk profile, while sellers resist repricing.”

Beginning in early 2023, the bid-ask spread became a defining feature of the marketplace. Sellers often held pricing expectations 100 to 200 basis points in cap rate above where buyers were willing or able to transact.

Over time, that gap has meaningfully narrowed — by late 2025, spreads have compressed to roughly 50 to 100 basis points, making it far easier to bridge both sides of the transaction. While many deals are still driven by motivated or time-sensitive sellers, transaction volume has noticeably improved over the past six months.

Although we may never return to the velocity of 2022, the market continues to move in the right direction, with additional momentum expected as loan maturities from the 2021–2022 cycle prompt further capital recycling in the years ahead.

Inflation and the Broader Economic Picture

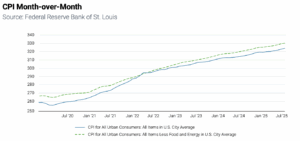

September data showed headline CPI up 0.3% month-over-month and 3.0% year-over-year, with core inflation matching that pace. This could be characterized as a one-time adjustment rather than a continuing cycle, forecasting CPI to hold in the upper-3 percent range through 2026 before gradually easing. That trajectory supports the Fed’s cautious easing stance while keeping real yields positive.

Recent tariffs have also contributed modest upward pressure to consumer prices, though their overall impact has been tempered by companies absorbing a portion of input costs to preserve demand and market share.

This dynamic has softened short-term price increases but may extend the timeline for full cost pass-through, keeping inflation slightly elevated in the near term. The effect this brings to real estate markets – more uncertainty.

Service-sector inflation remains elevated due to persistent labor decline, yet steady wage growth has helped sustain consumer spending — particularly within necessity-based retail and daily-needs categories. While this dynamic keeps inflation from falling faster, it continues to support healthy tenant performance and retail sales.

Retail Fundamentals Remain Exceptionally Strong

Retail continues to be an anchor of stability within the commercial real estate landscape. Competition for high-quality retail assets remains intense, particularly among well-capitalized private and institutional buyers. Many owners who lack a strategic reason to hold certain properties are recognizing that now may be an opportune moment to capitalize on heightened demand and favorable pricing dynamics, especially for assets that align with institutional investment criteria. National vacancies stand near 4.2 percent, the lowest level this century, while rent growth remains positive. Construction completions in Q2 totaled just 7.2 million square feet, a fraction of historical norms, reinforcing landlord leverage and supporting valuation stability.

Institutional sentiment echoes that strength. The Illinois Municipal Retirement Fund and Mississippi PERS have both committed new capital to retail-focused strategies from TA Realty and Newport Capital Partners, reinforcing long-term confidence in essential retail.

Meanwhile, new entrants such as Curbline, CenterSquare, and Bond Street have collectively committed billions toward unanchored necessity retail — the so-called “Amazon-proof” segment that has proven remarkably resilient post-COVID.

Across anchored and unanchored centers, retail assets with stable cash flow and manageable capital needs remain the most balanced sector in commercial real estate. In a time of uncertainty, these qualities remain valuable.

The Opportunity for Disciplined Private Capital

Periods like this tend to frustrate sellers and challenge buyers, yet they also give rise to selective opportunities in the marketplace. While we are not in a full buyer’s market, the environment is gradually shifting in that direction — creating advantages for well-capitalized, private investors able to act decisively.

As John Chang observed, “The window of opportunity is already here.” Stabilized pricing, moderate inflation, and a clearer rate path suggest that well-capitalized buyers have a chance to secure strong long-term yields before spreads compress again in 2026.

Amid volatility in the broader economy and equity markets, real estate continues to stand out as a relative safe haven — offering stable cash flow, tangible value, and the potential for improved capital costs as monetary policy continues to ease. This positions the current environment as one of recalibration rather than reset.

Retail real estate, particularly in the Southeast and Sunbelt, remains the most balanced sector in CRE.

Population growth, limited new construction, and steady consumer spending continue to support strong NOI performance even as other asset classes struggle with oversupply. For investors willing to transact in this environment — where leverage is limited but fundamentals are solid — there is room to acquire necessity-based centers at attractive basis levels before the market transitions.

Looking Forward: Stability, Not Complacency

As investors adapt to this evolving environment, the emphasis is shifting from timing the market to understanding it — identifying stable income opportunities amid broader uncertainty. Despite the noise — from a month-long government shutdown to shifting inflation data — the broader message is one of stabilization. The Fed’s decision to end QT removes a major drag on long-term rates; inflation appears contained, and transaction velocity, though below equilibrium, continues to improve.

Uncertainty will persist, and so will differing opinions on the timing and magnitude of future cuts. But the direction of travel is clear: toward normalization. For investors and brokers who stay active — reassessing valuations, underwriting conservatively, and engaging with motivated capital — the next phase of this cycle could present some of the best buying opportunities since 2021.

Next Steps

If you’re curious how your shopping center’s value has shifted in today’s environment — or would like a complimentary valuation and strategy discussion — I’d be happy to serve as a resource. Likewise, if you’re exploring acquisitions or want perspective on sourcing opportunities, feel free to connect directly. The path forward may be uncertain, but it’s navigable — and in today’s market, informed action is the ultimate advantage.