Capital stacking is the framework investors, developers, and lenders use to understand the order of funding sources in commercial real estate deals. It organizes the layers of debt and equity that finance a project, showing who gets paid first, who takes the most risk, and how returns are distributed.

For investors, sponsors, and capital providers, understanding the capital stack is essential. It determines risk exposure, potential returns, and negotiation leverage.

What Is “Stacked Capital”?

The term “stacked capital” refers to the complete structure of layered funding. Unlike a single-source loan, stacked capital combines debt and equity into a cohesive financing plan. This approach provides flexibility, diversified risk, and tailored solutions for sponsors and investors.

What Does Capital Stacking Mean?

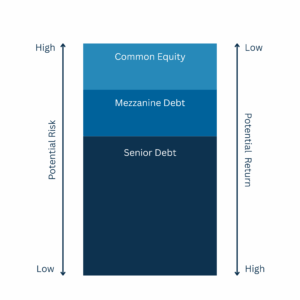

Capital stacking describes how different types of financing are organized based on their level of risk and repayment priority. Each layer carries its own return expectations and repayment order. In simple terms, the capital stack is both a financing structure and a risk ladder.

Lower layers, such as senior debt, carry lower risk, lower return, and the highest repayment priority. Upper layers, such as common equity, assume the greatest risk but also hold the highest potential reward. This organization matters because it impacts the cost of capital, investor returns, and how resilient a project is during downturns.

Key Components of a Capital Stack

A capital stack is typically built from four primary layers, with variations depending on the deal and market conditions. Each layer has its own cost, priority, and role in balancing risk and return.

- Senior Debt is the foundation of most deals. Usually provided by banks or institutional lenders, it carries the lowest cost of capital and the highest repayment priority. In many commercial real estate transactions, senior debt covers roughly 50–65% of total project value and is secured by the property itself.

- Mezzanine Debt comes next in priority. It fills the financing gap when a lender limits leverage, offering sponsors additional capital without issuing more equity. Because it’s subordinate to senior debt, mezzanine carries higher interest rates and may include equity participation or conversion rights to reward added risk.

- Preferred Equity is a hybrid layer between debt and equity. Investors in this layer receive a fixed or preferred return before common equity distributions, often with limited control over daily operations. It offers higher potential returns than debt but greater stability than pure equity, making it attractive for investors seeking predictable income with some upside potential.

- Common Equity is the top of the stack and represents true ownership, such as the sponsor and outside investors. It carries the most risk because it’s repaid last, but it also captures all remaining profits once other layers are satisfied. If the project performs well, common equity sees the greatest reward.

Other variations may include tax credit equity (common in affordable housing), joint venture equity where partners pool resources, or bridge financing that temporarily fills gaps until permanent funding is secured.

Example

Consider a $10 million property acquisition with multiple financing layers:

| Layer | Amount | % of Capital Stack | Risk/Return Profile |

| Senior Debt | $6M | 60% | Lowest risk, first repayment |

| Mezzanine Debt | $2M | 20% | Moderate risk, higher return |

| Common Equity | $2M | 20% | Highest risk, residual profits |

This illustration highlights how debt and equity combine to finance a deal. Every dollar of equity is leveraged by lower-cost debt, but the higher in the stack, the greater both the risk and the potential return.

Capital stacks vary by project and market conditions. For instance, if a lender caps senior debt at 60% LTV, the sponsor may need mezzanine financing or additional equity to close the deal. Historic tax credits or Opportunity Zone equity can also be layered into the stack. In other situations, developers rely on short-term bridge loans during construction, refinancing into permanent debt once the project stabilizes.

Benefits and Risks of Capital Stacking

The capital stack offers several benefits. By combining lower-cost senior debt with higher-return equity, it lowers the blended cost of capital and enhances potential returns. It also gives sponsors flexibility to bridge financing gaps and design tailored structures that appeal to multiple investors.

At the same time, risks exist. Mezzanine and preferred equity layers are more expensive, and repayment waterfalls can be complex. In downturns, equity is the most exposed, facing the possibility of a total loss if revenues cannot cover debt service.

Mitigating these risks requires discipline: conservative leverage ratios, stress testing assumptions, and clear, transparent waterfall models.

Capital Stacking for Business Funding

Developers and sponsors use capital stacking strategically. It allows them to balance equity dilution against borrowing costs, match financing terms to project stages, and tailor risk profiles to different investors. A core stabilized asset might rely heavily on senior debt, while a value-add property could involve more mezzanine financing and equity. Opportunistic projects, by contrast, often demand substantial equity with flexible secondary financing.

By layering capital thoughtfully, sponsors can scale portfolios, syndicate deals, and manage investor expectations more effectively.

How Sands Investment Group Structures Capital Stacks

SIG’s philosophy is to align interests, protect downside equity, and optimize blended cost of capital. For example, on a $15 million mixed-use development, the team structured a capital stack with 60% senior debt, 15% mezzanine financing, and 25% equity. The repayment waterfall was designed to prioritize stability, shielding equity from early losses while capping mezzanine returns to control overall cost. This thoughtful structuring attracted multiple investors and reduced financing risk across the deal.

Frequently Asked Questions

What does capital stacking mean?

It is the arrangement of financing layers—debt and equity—by risk and repayment priority. For businesses, it is the use of layered financing—loans and equity—to fund growth while balancing risk, return, and control.

What is an example of a capital stack?

A $10M deal with $6M senior debt, $2M mezzanine, and $2M equity.

What is stacked capital?

The complete structure of debt and equity that funds a project.

Who gets paid first?

Senior debt holders are repaid first, followed by mezzanine and preferred equity, with common equity paid last.

Conclusion

Capital stacking is more than a financial framework; it is the foundation of deal structuring in commercial real estate. For investors, it provides insight into risk and return. For sponsors, it offers a tool to attract capital, control costs, and align stakeholder interests. For both, understanding the nuances of the stack is critical to long-term success.

Connect with the Capital Markets team to explore tailored capital stacks that support your investment strategy.

IMPORTANT INFORMATION

Sands Investment Group and its affiliates do not practice law and do not give legal, tax, or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. You should consult your own tax, legal, and accounting advisors before engaging in any transaction.